So much more Graduates To-be Recognized During the 2016

The newest recommendations on the knowledge loans will make it easier for present graduates – and many others that have student debt – to obtain recognized within the 2016.

Productive instantaneously, education loan fee data has alleviated. FHA loan providers will today fool around with down monthly payment rates to own deferred student education loans.

Having reduced financial pricing and easier qualification having college students, 2016 are growing to be a stellar year to possess younger home buyers.

Student education loans Continue Of numerous Graduates Away from To shop for

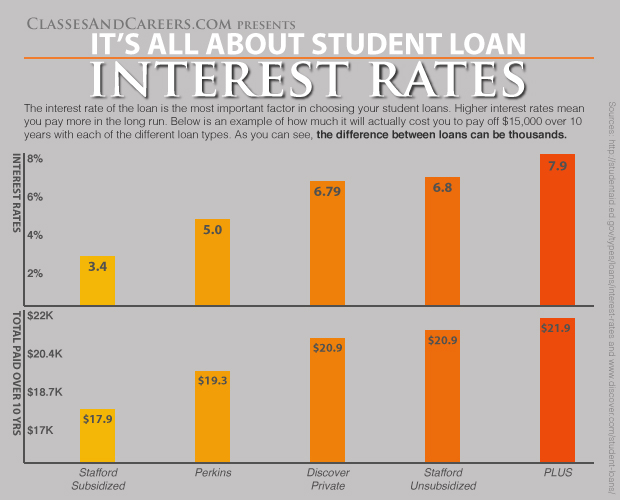

An average student loan debt an effective 2015 scholar is all about $thirty five,000 getting a beneficial bachelor’s degree, $51,000 to own an effective Master’s and you can $71,000 to possess a Ph.D.

Those individuals wide variety are popular up, also. When you look at the 2012 pupils sent a median loan amount off $26,885pare one to simply $a dozen,434 20 years before.

Education loan obligations commonly weighs in at down graduates for decades. There are plenty of forty-year-olds which can be nevertheless settling student education loans. To them, education loan loans has actually spanned an entire age group.

Using code transform out-of Casing and you may Urban Innovation (HUD), the latest agencies you to definitely oversees the favorite FHA home loan program, graduates are certain to get an easier time qualifying for a home loan.

Here you will find the FHA Student loan Signal Change

Of many 2016 mortgage applicants with education loan obligations will dsicover one to the likelihood of to purchase property is actually greatly improved.

Of many recent graduates features deferred figuratively speaking. They are certainly not necessary to generate payments until a certain amount of time just after graduation. This provides all of them time for you start their jobs, and start getting a payday.

That is a beneficial arrangement. Nevertheless when this type of college grads make an application for a home loan, the financial institution must factor in coming education loan payments. Usually, zero payment information is readily available.

Using 2016 status, loan providers have a tendency to estimate deferred student loans at just one percent away from the borrowed funds equilibrium in the event that no fee data is readily available. That it effortlessly halves new perception away from deferred student education loans in your mortgage software.

Keep in mind that so it rule pertains to student education loans having and this no fee information is offered. In case your genuine payment appears towards the credit report otherwise loan paperwork, the greater of your own actual commission or step 1% of harmony might possibly be useful for qualification objectives.

Yet ,, getting applicants which are unable to file a future education loan payment, so it relatively brief alter may have deep outcomes acceptance.

How Code Alter Can play Aside To you

Need this example. A recent graduate discovers a career straight-out out of university. She helps make $4,000 monthly. Their unique complete monthly payments in the event the she shopping property could be $step 1,five hundred 30 days along with their unique future domestic commission, an automible fee and you will a charge card.

Under previous guidelines, their own estimated fee might be $400 four weeks. So it sets their personal debt-to-money ratio at a level that’s too high is recognized.

Under the latest rules, the lender prices her student loan commission at just $2 hundred, otherwise 1% of their loan equilibrium. Their personal debt-to-income is now in this acceptable levels, and she actually is approved getting a mortgage.

$30,000 within the college loans: $3 hundred 30 days reduced estimated costs $fifty,000 into the figuratively speaking: $five hundred 30 days reduction in estimated payments $100,000 when you look at the college loans: $1,000 per month loss in estimated repayments

Brand new applicant’s to purchase electricity is actually increased by amount the projected payment decreases. To phrase it differently, a home visitors with $fifty,000 during the figuratively speaking is now able to end up being recognized having a home fee that’s $500 highest.

Just remember that , in case the genuine percentage is obtainable, the financial institution uses that amount, if it is higher than the brand new step 1% estimate.

Additionally, if the step 1% of one’s loan equilibrium is greater than the actual commission into loan data or your credit history, the financial institution have to use the you to-% contour.

This new FHA rules up to deferred college loans, but not, usually unlock homeownership chances to a complete inhabitants that was secured regarding home ownership simply days ago.

FHA Guidance Could Change Renters To the People When you look at the 2016

First-time customers represent a typically reasonable portion of this new . Based on , the new people made-up 32 % of all home buyers.

That is the second-lower reading since a home trade organization been putting together investigation in the 1981. First-big date family consumer accounts haven’t been this low because the 1987.

Ever-rising rents and all taxation benefits associated with homeownership have a tendency to spur tenants to a lot more you should consider buying a property. And you will student loans might no expanded end them out of going right on through in it.

This opens up an unusual chance for home buyers: latest students are able to afford more domestic at a lower price thanks to lowest cost.

What are Today’s Costs?

For those who have higher student loan personal debt, think an FHA financing, with recently loosened the advice doing estimated mortgage costs.

Rating a speed offer if you find yourself cost is actually lowest and you will assistance are accommodative. You might be surprised at the home your qualify to order at this time read this post here.